Have you ever looked at your pay stub and wondered what "OASDI" means? This mysterious acronym appears on millions of paychecks across America, yet many workers don't fully understand what it represents or why such a significant portion of their earnings goes toward it.

OASDI tax is one of the largest deductions most employees will see on their paychecks throughout their working lives. Understanding what it is, how it works, and how it affects your take-home pay is essential for financial planning and retirement preparation. This comprehensive guide breaks down everything you need to know about OASDI tax in 2026.

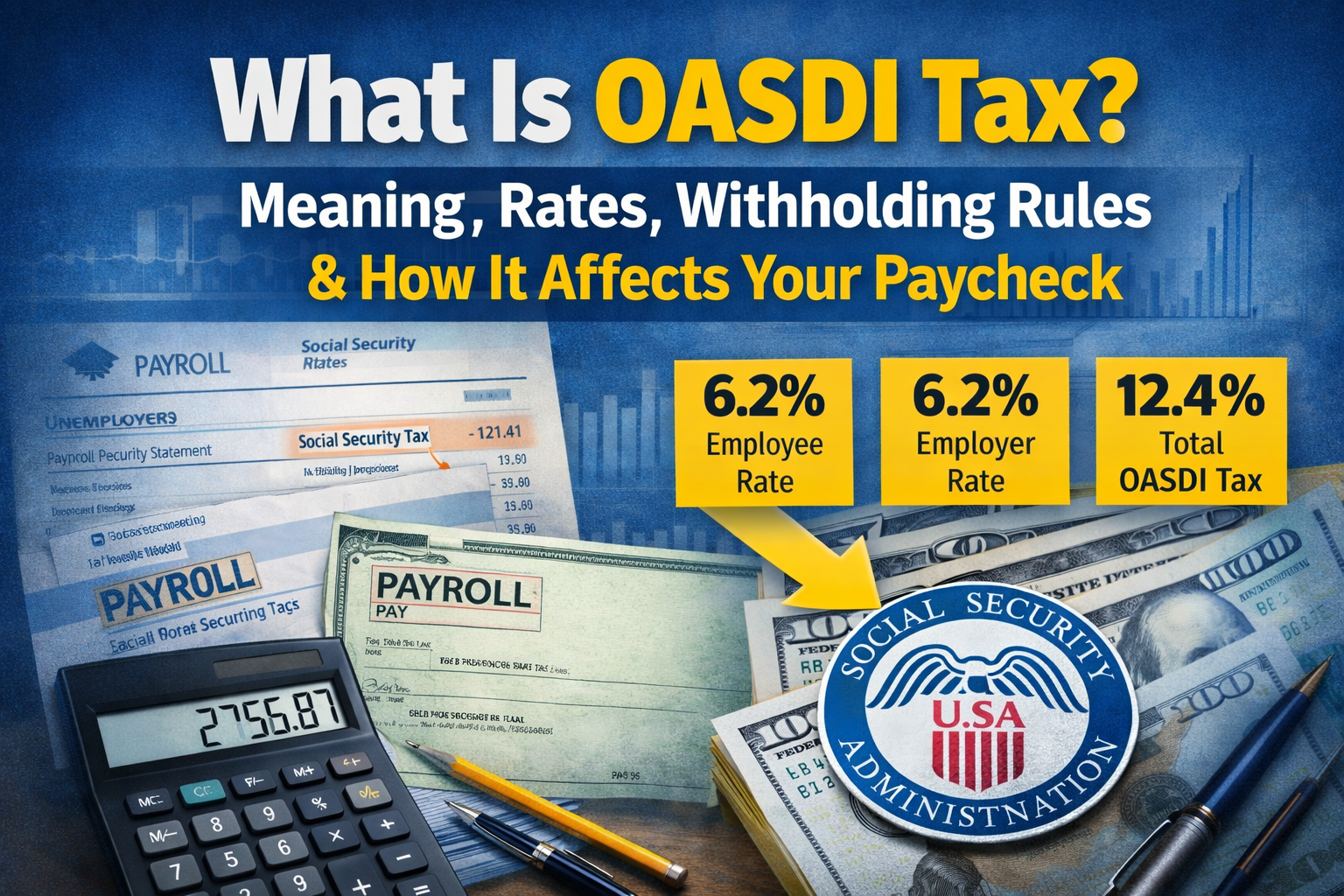

OASDI stands for Old-Age, Survivors, and Disability Insurance. It's the official name for Social Security tax, which funds the Social Security program that provides benefits to retired workers, disabled individuals, and survivors of deceased workers.

The OASDI tax was established through the Social Security Act of 1935 as part of President Franklin D. Roosevelt's New Deal programs. The goal was to create a social insurance program that would provide financial security for Americans in retirement, during disability, or after the death of a wage earner.

Old-Age Insurance: Provides retirement benefits to eligible workers starting at age 62 (with reduced benefits) or full retirement age (currently 67 for those born in 1960 or later).

Survivors Insurance: Provides benefits to family members of deceased workers, including spouses, children, and dependent parents.

Disability Insurance: Provides benefits to workers who become disabled and can no longer work, along with their eligible family members.

When you look at your pay stub, you'll often see OASDI and Medicare listed separately, though together they make up what's commonly called "FICA taxes" (Federal Insurance Contributions Act).

OASDI Tax:

Medicare Tax:

While both fall under FICA, they serve different purposes and have different rules. OASDI specifically funds Social Security, while Medicare tax funds healthcare for those 65 and older.

Understanding the current rates helps you calculate how much of your income goes toward Social Security.

The OASDI tax rate for employees is 6.2% of gross wages, up to the wage base limit.

Employers also pay 6.2% of each employee's gross wages, matching the employee contribution.

Self-employed individuals pay the full 12.4% (both the employee and employer portions) on net self-employment income up to the wage base limit. However, they can deduct half of this amount (the employer portion) as a business expense on their tax return.

The wage base limit is the maximum amount of earnings subject to OASDI tax in a given year. For 2026, this limit is expected to be approximately $176,100 (subject to official announcement by the Social Security Administration).

Once your earnings exceed this threshold during the calendar year, you stop paying OASDI tax on additional income for the remainder of that year. This means high earners pay OASDI tax only up to this cap, while Medicare tax continues on all earnings.

OASDI tax is withheld directly from your paycheck by your employer before you receive your wages. This is known as payroll tax withholding.

1. Gross Pay Calculation: Your employer calculates your gross wages for the pay period.

2. OASDI Tax Calculation: The employer multiplies your gross pay by 6.2% to determine the OASDI tax amount.

3. Withholding: This amount is deducted from your paycheck along with other taxes and deductions.

4. Employer Match: Your employer simultaneously pays an additional 6.2% directly to the government.

5. Remittance: Your employer sends the combined amount to the IRS regularly (typically monthly or semi-weekly depending on business size).

If you earn $5,000 in gross wages for a pay period:

Your take-home pay would be reduced by $310 (plus other taxes and deductions).

Let's say you earn $200,000 annually. Once your year-to-date earnings reach approximately $176,100 (the 2026 wage base limit):

This creates a nice end-of-year "bonus" for high earners who hit the cap before December.

The impact of OASDI tax on your take-home pay is significant. Let's examine how it affects workers at different income levels.

For someone earning $40,000 annually:

For someone earning $75,000 annually:

For someone earning $250,000 annually (assuming $176,100 wage base):

As you can see, the wage base cap means higher earners pay a smaller effective OASDI tax rate on their total income compared to lower and middle-income workers.

Your employment status determines how you pay OASDI tax.

Most workers are W-2 employees who have OASDI automatically withheld from each paycheck. The process is straightforward and requires no action on your part beyond reviewing your pay stub for accuracy.

Self-employed workers, independent contractors, freelancers, and gig economy workers pay self-employment tax, which includes both the employee and employer portions of OASDI.

How it works:

Example for self-employed: Net self-employment income: $80,000

If you work for multiple employers during the same year, each employer withholds OASDI tax independently. This can result in over-withholding if your combined earnings from all employers exceed the wage base limit.

What to do: When you file your tax return, the IRS will calculate if you overpaid OASDI tax and issue a refund for the excess. Report the overpayment on Form 1040, Schedule 3.

Nannies, housekeepers, and other household employees are subject to OASDI tax if they earn more than $2,700 annually (2026 threshold). Household employers must withhold and remit these taxes using Schedule H.

Generally, no. OASDI tax is mandatory for most workers. However, limited exceptions exist:

The rate (6.2%) has remained constant for many years, but the wage base limit increases annually based on changes in the national average wage index. This means the maximum OASDI tax you can pay increases most years.

OASDI tax isn't refundable in the traditional sense. Instead, you earn Social Security credits toward future benefits. For 2026, you earn one credit for each $1,730 in covered earnings (up to four credits per year). You need 40 credits (10 years of work) to qualify for retirement benefits.

The benefits you receive in retirement are based on your highest 35 years of earnings, adjusted for inflation.

Yes and no. Everyone pays 6.2% on wages up to the cap, but because of the wage base limit, high earners pay a lower effective rate on their total income.

This regressive element has been a subject of policy debates. Some argue for raising or eliminating the cap to ensure program solvency, while others oppose increasing the tax burden on high earners.

Understanding where your OASDI tax goes helps clarify why this deduction matters.

OASDI taxes flow into two trust funds:

These funds invest in special U.S. Treasury securities and pay benefits to current beneficiaries. This is a "pay-as-you-go" system where current workers fund current beneficiaries.

The Social Security Administration tracks your earnings and OASDI tax payments throughout your career. Your future benefit amount is calculated based on your 35 highest-earning years (adjusted for inflation).

You can view your earnings history and estimated benefits by creating an account at SSA.gov.

Social Security uses a progressive formula that replaces a higher percentage of pre-retirement income for lower earners:

(These are 2026 bend points and may change annually)

You may have heard concerns about Social Security running out of money. Here's what that really means:

According to the Social Security Trustees Report, the combined OASI and DI trust funds are projected to be depleted around 2034-2035. This doesn't mean benefits stop entirely—incoming OASDI taxes would still cover approximately 75-80% of scheduled benefits.

Several factors contribute to the funding challenge:

Policymakers have discussed various options:

While changes are likely needed to ensure long-term solvency, Social Security remains one of the most stable and reliable government programs.

Since you're paying OASDI tax throughout your career, you'll want to maximize your eventual benefits:

Benefits are based on your highest 35 years of earnings. Working fewer years means zeros in the calculation, reducing your benefit. Working more than 35 years can replace lower-earning years with higher ones.

Every month you delay between full retirement age and 70 increases your monthly benefit by approximately 0.67%.

Review your Social Security statement annually to ensure all earnings are correctly recorded. Report any discrepancies immediately, as there are time limits for corrections.

Married couples have additional claiming strategies that can maximize household benefits. Survivor benefits can be particularly valuable for protecting lower-earning spouses.

OASDI tax is just one piece of your overall tax and retirement planning puzzle.

Between OASDI (6.2%) and Medicare (1.45%), employees pay 7.65% in payroll taxes, while employers pay a matching amount. Self-employed individuals pay the full 15.3%.

Add federal income tax, state income tax (in most states), and other potential deductions, and your total tax burden can be substantial. Understanding each component helps you plan effectively.

While OASDI tax funds your Social Security benefits, these benefits typically replace only 40-50% of pre-retirement income for average earners. Financial advisors generally recommend additional retirement savings through:

Working with financial professionals or utilizing offshore tax preparation services can help you optimize your overall tax situation, including understanding how OASDI tax fits into your comprehensive tax strategy. Proper planning ensures you're taking advantage of all available deductions and credits while meeting your OASDI obligations.

Understanding your pay stub helps you verify OASDI withholding accuracy.

Earnings Section:

Deductions Section:

Summary Section:

Check that OASDI withholding stops once your year-to-date earnings exceed the wage base limit. If you notice continued withholding beyond this point or other discrepancies, contact your payroll department immediately.

OASDI tax rules evolve over time. Staying informed helps you plan effectively.

The wage base limit has increased steadily. In 2023, it was $160,200; in 2024, $168,600; in 2025, approximately $172,200; and is expected to reach around $176,100 in 2026. This represents significant increases that affect high earners.

Congress periodically considers Social Security reforms that could affect OASDI tax:

Stay informed about legislative discussions that might affect your tax burden and future benefits.

Understanding OASDI tax empowers you to make informed financial decisions:

The OASDI tax you see deducted from each paycheck represents an investment in your financial security during retirement, disability, or for your survivors. While the immediate impact on your take-home pay is noticeable, the long-term benefits provide crucial financial protection that most Americans will eventually rely on.

By understanding how OASDI tax works, monitoring your earnings record, planning your retirement timing strategically, and building additional retirement savings, you can maximize the value of your lifetime OASDI tax contributions and ensure a more secure financial future.